The first greenfield project of its kind on the UKCS, Tolmount Main has united three very different companies to create a new blueprint for field development.

Holding around 1 trillion cubic feet (tcf) of gas, the Greater Tolmount Area is one of the largest prospects on the UK Continental Shelf (UKCS). Despite its sizable resource however, the path towards development has not always been smooth.

Located across Blocks 42/28c, 42/28d and 42/28e, around 40 miles off the Yorkshire coast, the southern North Sea prospect was first awarded to Dana Petroleum in 2005. Early exploration efforts – both by Dana and later under E.ON, which farmed in with a 50% operator stake – failed to make much progress, with drilling campaigns plagued by rig issues and well collapses. It wasn’t until 2011, after an extensive redesign, that the partners successfully identified and flow-tested a gas column in the Lower Leman Sandstone Formation, and a further two years before appraisal wells confirmed the extent of the resources.

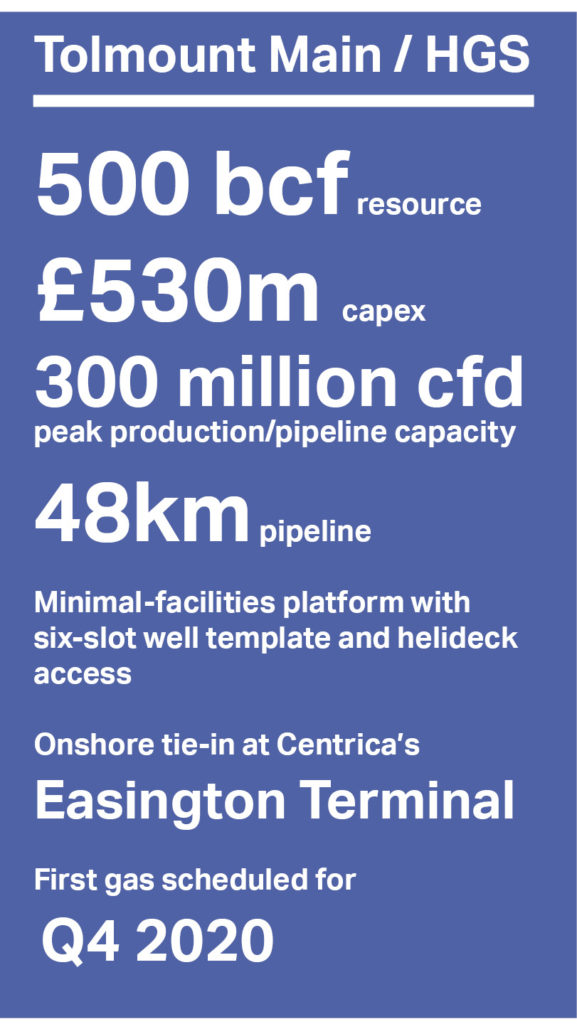

Compared with those early days, the project’s fortunes now look very different. The fully appraised Tolmount Main gas field is estimated to hold around 500 billion cubic feet (bcf) of recoverable resources and forms the centrepiece of an award-winning partnership between E&P companies and a pioneering midstream infrastructure business. Having reached a final investment decision (FID) in August 2018, Tolmount is now on course to produce first gas by late 2020 and, at its peak, will produce up to 300 million cubic feet per day (cfd).

Alongside the ongoing co-operation between licence partners Dana and Premier Oil – the latter took on its 50% operator stake during the acquisition of E.ON E&P’s UK portfolio in 2016 – the addition of energy infrastructure company Kellas Midstream (formerly known as CATS Management) has been instrumental in bringing the project to fruition. In a first-of-its-kind arrangement, a separate joint venture (JV) between Dana and Kellas has mobilised investment for the creation of a new minimal facilities platform and 48km pipeline known collectively as the Humber Gathering System, or HGS, which will carry gas to the Centrica Storage-operated Easington terminal.

It is the interlocking nature of these ventures that makes this project unique. “It went from one 50/50 partnership to two 50/50 partnerships,” Kellas Midstream’s operations director Alan Murray explained to Wireline. “The Tolmount field operators remained the same, but Humber Gathering System Limited (HGSL), a Kellas entity formed specifically for this project, and Dana became partners in the infrastructure.”

Under the terms of the deal, Kellas and Dana will jointly fund, construct and own the infrastructure, with Kellas assuming operatorship. Once production begins the venture will be paid a tariff for gas transportation, adjusted based on the volumes delivered. Premier, meanwhile, is responsible for overall project management, and the delivery and completion of wells – but with a significantly reduced capital commitment than would otherwise have been necessary to realise the project.

This kind of co-operation between producers and infrastructure owners opens new routes for future UKCS developments and new perspectives on how Maximising Economic Recovery (MER UK) can be delivered. Wireline sat down with the HGS/Tolmount partners to find out more about how the partnership was created, and whether it could be replicated in future.

“The convention that we’ve broken here is that someone else can pay for that infrastructure and the operator therefore has more money to drill more wells, shoot more seismic and do more exploration.”

On good terms

An onshore tie-in had been the preferred export route for Tolmount for some time, although the project did require the right combination of partners. Dana Petroleum developments manager Eric Bell noted that: “We had ruled out tying into offshore infrastructure and were focused on coming to the east coast, around the Dimlington or Easington terminal infrastructure. That’s when Premier came in, and we had a period of reflection before we advanced our FEED activities and sorted out the ultimate offtake which was the critical feature to get the project going.”

With this agreed, the next stage was to identify an infrastructure manager. “At that stage Premier was looking for ways to unlock this development and had considered various ways of making this happen – as a farm-down, a farm-out, raising more capital – and they landed on wanting to get involved with one of the infrastructure companies,” Alan added. Conversations between Premier and Kellas Midstream began in early 2017, building on a pre-existing relationship established via Premier’s operated interest in the Huntington field, which exports gas through Kellas’ Central Area Transmission System (CATS) pipeline, and a partnership was established.

At the same time, Kellas conducted parallel discussions with Dana regarding the creation of a separate venture which would be responsible for building, installing, commissioning and operating the platform and pipeline infrastructure. This culminated in all three partners signing heads of terms agreements in September 2017 – a mere six months since conversations began in earnest. “It was a lot done in a short space of time,” concurred Premier Oil development projects manager, Craig Matthew, but with several years of FEED and scoping already complete, the parties were keen to identify and enact a swift route to development.

This positive, early engagement proved to be a sound bedrock for the rest of the development process. “We spent a lot of time on those heads of terms,” Alan added. “That’s one of the lessons we have picked out – getting those principles nailed down early – and we stuck to them right the way through.”

Under the agreement Premier would continue as the joint development operator and not only drill, complete and manage the four development wells (subcontracted to Ensco), but also project manage the construction of the independent infrastructure. The preservation of Premier’s ability to oversee the project and retain much of the traditional elements of operator-led decision-making and control proved a key decider in moving ahead, Craig noted.

Total development costs for the project stand at around £530 million, with Kellas funding approximately £175 million, and Premier around £90 million. As a partner in both the upstream and midstream JVs, Dana will match each of these respective contributions, totalling around £265 million.

In addition to future revenues from gas sales, the project presents a significant opportunity for the UK supply chain; 50% of that expenditure will be committed to UK companies, covering the platform, pipeline and terminal FEED engineering, and modifications to the Easington terminal to enable gas receival and processing.

The midstream model

Although common in regions like onshore North America, the introduction of midstream operators in the UKCS is relatively novel; with few exceptions, the tendency is for pipelines to be commissioned and built by the field operators themselves. The move towards a leasing model for greenfield developments, similar to those used in FPSO-based projects, opens up a new avenue for North Sea producers.

Being ostensibly unique – “We believe that it is the first independently owned greenfield offshore pipeline in the UK,” Alan confirmed – this approach presented challenges in writing and navigating commercial arrangements, but was important in unlocking an opportunity that may otherwise have been unavailable. “Upstream E&P companies generally want to invest in drilling wells and shooting seismic and producing their hydrocarbons. They invest in infrastructure as a means of getting that hydrocarbon to a point where they can sell it, and the cost of that infrastructure is a big chunk of the project,” he expanded. “The convention that we’ve broken here is that someone else can pay for that infrastructure and the operator therefore has more money to drill more wells, shoot more seismic and do more exploration.”

“From an MER UK perspective, having infrastructure owners rather than field operators owning that infrastructure, it does allow the potential to create new hubs and to get more out of the ground in these areas.”

“The attraction of this model for Premier is that we retain our 50% ownership,” added Craig. “With other models like farming down you dilute your stake in the hydrocarbons and we weren’t really interested in doing that. It’s a very attractive prospect and essentially in boe, [is] the same for us as our Catcher development, so we don’t really want to dilute that value.”

The construction of the agreement also changes the project’s payback terms. In addition to significantly reducing the capital budget needed to get the project in motion, Craig noted that it provided a reasonable measure of tax efficiency. “It’s a lot better to have the expenditure down the operating curve rather than up front. It has worked for us in a lot of respects, and if we hadn’t come up with this arrangement it’s hard to see that the project would have actually moved forward,” he added.

It is also a gateway opportunity for Kellas Midstream. Although built to accommodate peak production of up to 300 million cfd from Tolmount Main, the HGS platform and pipeline was conceived with overcapacity in mind, allowing for potential expansion of the field and surrounding area. “One of the important features was that the infrastructure was not intended to be Tolmount-specific. The idea was that it should be a system that had potential to bring in either additional Premier-Dana opportunities that we hope are in the area, and third parties,” Eric noted. “That was an attraction for Kellas – they didn’t just want a single development, they were hoping it would provide an opportunity that the bigger pipeline and higher flow rates bring.”

More than that, the setup of the HGS infrastructure – which includes investment in additional risers and J-tubes – enables lower field development and tie-in costs for those future projects. According to Kellas, the pipeline could become a hub for southern North Sea production for at least the next 20 years.

This approach could be transformative for other areas of the UKCS. “From an MER UK perspective, having infrastructure owners rather than field operators owning that infrastructure, it does allow the potential to create new hubs and to get more out of the ground in these areas,” Craig said. “If there is another party in there that is a bit broader-minded, then perhaps there is a bit more of a future for some parts of the North Sea if more projects are done this way.”

Common ground

Despite the partners’ commitment, the path to project sanctioning in August 2018 was not without its challenges. The largest, according to Kellas’ Alan Murray, was the sheer volume and complexity of commercial agreements. While there was no silver bullet to overcoming this, he praised the work of commercial teams across the project who worked diligently to create terms that met the needs of all three parties. “It took a little bit of mapping out as to what we needed to do. All of the normal commercial agreements had to be created… [We] had to add additional agreements to manage the hand off between the Tolmount field to the HGS platform, but it wasn’t outwith the wit of man to do it, it just took a little bit of time.”

This was aided by regular engagement with a management steering committee and – crucially – an open-book economic model between all three companies, which removed many of the traditional barriers encountered during this type of negotiation.

“We spent a lot of time on having a set of fully termed agreements at FID. That was something we were all keen to do and it was a huge amount of work up front for our commercial folks, but going forward the pressure is off and we have aligned how things are going to work in future,” he added.

“I think for all parties it just provides that level of clarity and commitment that allows us to go off and manage the project now, without the distractions of ongoing commercial negotiations,” echoed Premier’s Craig Matthew. “You have to find common ground, you have to find ways that work for all parties, and that was exemplified in the effort that went in pre-FID here.”

There was also a late and significant change in project scope. In late 2017, some months into discussions, the choice of terminal moved from Dimlington to Easington, creating a ripple effect through the project. Agreements had to be changed and new parties brought into the contracting process, but again the group’s commercial teams worked to ensure the course was stayed.

A final learning experience for the group was how it communicated this blueprint to investors, supply chain and to UK regulators, including the Oil and Gas Authority (OGA), Department for Business, Energy and Industrial Strategy (BEIS), Health and Safety Executive (HSE) and Offshore Petroleum Regulator for Environment and Decommissioning (OPRED). All characterised the process as constructive and positive, with Dana’s Eric Bell adding that: “I think the OGA were very open to new ideas, but we had to demonstrate it… I think if they saw MER was not being delivered then we would have had more difficulties but fortunately we were able, I believe, to show that it was being served.”

MER to come

Breaking new ground is never straightforward, but in this case the hard work and diligence of the HGS/Tolmount partners has also been noticed by the wider industry. In November 2018 the project was awarded an MER UK Award at the annual Oil & Gas UK Awards, in recognition of the project’s contribution to these strategic goals.

Reflecting on why HGS/Tolmount was chosen, all felt that it was the spirit of co-operation that enabled the goals of MER to be met. “Collaboration is a bit of a buzzword that’s been around for a few years, and MER relies on collaboration,” Eric ventured. “I think you’ve seen the collaboration between three companies that had different objectives, and they created the alignment to deliver in what is quite a short period of time given the number of agreements and understandings that had to be demonstrated. I think [that] was one of the factors that we were viewed as having done well.”

Added Alan: “I think the award panel saw the relationship, the positivity and the “can-do” nature of this… It was all done positively – there were no barriers and we are colleagues, not competitors.” Indeed, that spirit has continued through FID and into execution – “Collaboration doesn’t stop at the sanction stage,” Craig assured.

“We see the HGS/Tolmount project as being directly replicable in other parts of the North Sea, in the UK side and Norwegian and Dutch sides. It has generated a lot of interest and we are actively speaking to a number of parties.”

At the time of writing, engineering and fabrication for the HGS infrastructure is well underway. Rosetti Marino cut first steel for the platform in December and “upwards of £20 million” in expenditure has already flowed through to the supply chain. Engineering and procurement of trees, wellheads and subsea pipeline have all begun, and according to a January operations update from Premier, first gas remains on schedule for the fourth quarter of 2020.

Beyond Tolmount Main, nearby prospects Tolmount East and Tolmount Far East – estimated to hold 220 bcf and 150 bcf of unrisked gas, respectively – are set for further scrutiny, with 3D seismic acquisition across the whole area planned for the first half of this year, as well as an appraisal well at Tolmount East in mid-2019. If successful, this could be developed either as a platform or subsea well and tied back into the Tolmount Main infrastructure, Craig confirmed.

With approval from regulators and accolades from peers, Tolmount marks something of a watershed moment in UKCS corporate collaboration. Kellas certainly is confident that a midstream-backed approach could be applied to other fields and developments in future – at home and abroad – given the right attitude and conditions. “We see the HGS/Tolmount project as being directly replicable in other parts of the North Sea, in the UK side and Norwegian and Dutch sides,” Alan confirmed. “It has generated a lot of interest and we are actively speaking to a number of parties.”

While all three representatives agreed that the model would not be suitable for every situation, they are hopeful that visibility of a project such as Tolmount may encourage others to think differently when it comes to offshore developments. “If we’re successful there may be others that see [this] as a possible mechanism that would allow them to do something different,” Eric suggested. “Bringing more infrastructure players into the development of the North Sea may offer something that might not appear if we all stayed traditional.”

Primarily though, Tolmount highlights that collaborative behaviour need not undermine a profitable outcome. In fact, it may prove to be the key that unlocks developments that would otherwise have been overlooked (or over-priced). For Kellas’ Alan Murray, it’s prime example of the right assets being in the right hands: “We have three completely different reasons for involvement, but one solution. It just shows you that businesses can have different motivators, but it can still result in projects moving forward.”